By James Bryan, Jessica Clempner, and Simon Low

This article was first published on April 6, 2020.

Editor's note: Oliver Wyman is monitoring the COVID events in real time and we have compiled resources to help our clients and the industries they serve. Please continue to monitor the Oliver Wyman Coronavirus hub for updates.

The novel coronavirus (COVID-19) is already having a profound effect on people’s lives and on the global economy. Retail banks have a central role to play in not just supporting customers and employees, but society as well.

Most banks have triggered their business continuity plans (BCP) and are grappling with the immediate impact of the pandemic and new ways of working. The structures put in place now will determine how individual banks – as well as entire communities – not only weather the storm, but also emerge stronger.

We know that the next three months are critical to the future of the retail-banking sector. Our work with banks in Asia, Italy, and Spain has given us insight into how the impact of the pandemic evolves. Our public policy and large-scale restructuring experience following previous crises (such as mortgage restructuring in Ireland and the US, and management of small- and medium-enterprises’ non-performing loans in Greece) has provided a perspective on how to operationally transmit policy to thousands of customers.

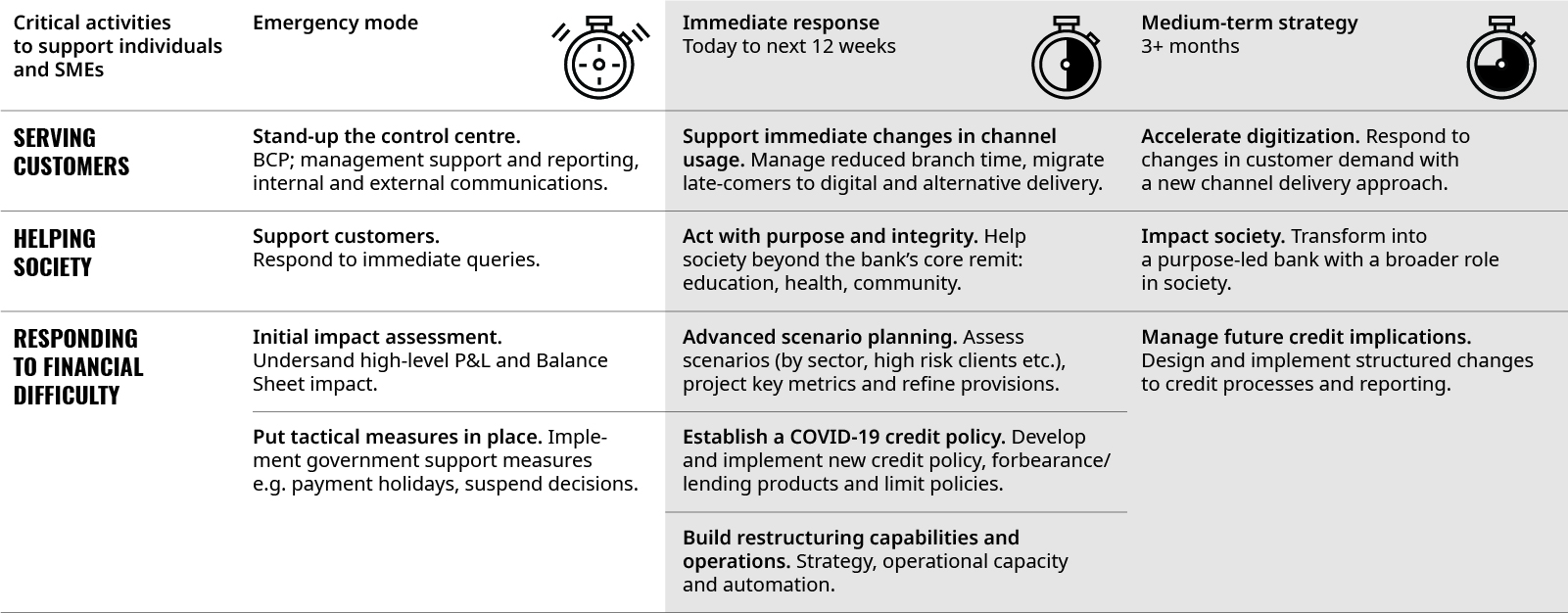

We see three key areas of focus: serving customers – ensuring access to critical services in the near term and accelerating the transition to digital beyond that; helping society – supporting customers and communities through the pandemic; and responding to financial difficulty – scenario planning, establishing a COVID-19 credit policy, and operationalizing restructuring capabilities.

Looking ahead, the pandemic is likely to have significant knock-on implications for the industry. Managing cost will be critical for banks to survive, requiring short-term cost management (e.g. limiting discretionary spend) and a better understanding of cost drivers and the new survival minimum to make more structural changes in the long term. New M&A opportunities will also likely emerge, as changing industry dynamics drive restructuring.

COVID-19 MANAGEMENT FRAMEWORK

SERVING CUSTOMERS

The first concern must be in delivering financial products and services to customers when they need them most. The first step is to establish a COVID-19 response center. Additionally, banks must react to rapid changes in channel usage in the short term and anticipate changes in customer demand that these shifts will drive in the medium term.

Support immediate changes in channel usage

The current situation is forcing people to change the way they live. To continue to provide for customers, a plan is needed for each banking product or service: a new in-person model, alternative delivery models (for example, at home), advanced ATMs, digital provisions, or halting the service. The impact on different customer segments needs to be thought through, particularly for latecomers who have not yet moved to digital, to make sure they are not left behind.

Take cash as an example. In some countries, exchanging notes is being seen as a potential source of infection for customers and employees. In contrast, contactless or mobile pay is more hygienic. Banks can accelerate the shift by encouraging the use of cards (for example, changing the fee or incentive structure), communicating the benefits, and working with businesses to reduce cash usage.

Accelerate digitization

Looking ahead, these unprecedented changes will shift customer demand permanently. Banks need to start planning to accelerate digitization and channel migration to respond to these behavioral changes. This means reviewing digital programs and reprioritizing capacity and capabilities. Practically, all activity should undergo a rigorous “start, stop, continue, accelerate” assessment.

HELPING SOCIETY

Individual banks, and the industry more broadly, have the opportunity and the responsibility to support society through this health crisis. To emerge stronger, it will be essential to think beyond the core business to support your customers and communities.

Act with purpose and integrity

Many customers will need help outside their basic financial needs. Actively encourage and empower employees to help customers beyond the bank: from education, to health, to supporting the community. One European bank, for example, has partnered with a digital-learning platform to provide free access to learning for customers’ children no longer able to attend school.

Impact society

In the medium term, this could be a turning point to jolt the organization and transform into a truly purpose-led bank. How a bank acts today will determine its future culture and reputation among the customers it serves. Purpose and societal impact should not be an afterthought, but a core part of how you navigate through the coming months, translating into business decisions, performance enablement, and key performance indicators.

RESPONDING TO FINANCIAL DIFFICULTY

A significant challenge will be to respond to the rapidly changing credit situation: increased demand for liquidity, worsening credit outlook for customers, government support programs, forbearance both with and without a government mandate, and the untested impact of new rules (such as IFRS 9). Initially, those worst affected are likely to be small businesses and the self-employed. But in three to six months, once initial forbearance initiatives fall away, this will extend to individuals.

Advanced scenario planning

Scenario analysis is critical in this uncertain environment, to consider macro-epidemiology and economy scenarios, as well as public-policy responses from supervisors, governments, and central banks. Integrated scenario results should be used to measure the effect on key performance metrics. Banks will need real-time simulators to assess the impact on credit, exposures, provisions, capital, and liquidity. Ensuring that strategies feed into business decision-making will be key to success.

Establish a COVID-19 credit policy

In addition to implementing immediate tactical responses, such as emergency lending for small and medium enterprises with cash-flow issues, and government support measures, a more refined COVID-19 response credit policy will need to be established. Initial basic client solutions will need to be quickly broadened into a more detailed suite of customer treatments and products.

Build restructuring capabilities and operations

Immediate response policies will need to be operationally transmitted to clients through decision-tree models, retuning the digital channel and removing any process blockers such as signatures or document delivery. Customers will need to be supported and educated on which options – whether government or bank – they are eligible for.

As the pandemic evolves, banks need to be prepared for the significant spike in customers in financial difficulty, which is likely to materialize in the next three to six months. Investment in restructuring and collections capabilities has historically been cyclical, and many banks are not prepared. A clear strategy and robust operating model will be essential, including decision trees, analysis and policy to support each node of the decision tree, data models, and automated data collections and case processing.

Manage future credit implications

Automation will be essential in handling the increased demand for credit, growing number of customers in financial difficulty, and shifts in channel usage. Accelerating digitization and smart lending capabilities will allow banks to make greater use of online technology to originate loans, use new data to make more efficient decisions, and deliver faster yes/no decisions. Investments made now in automating rapid response credit solutions will also improve business-as-usual lending activities.

CONCLUSION

Many retail banks are already rapidly responding to the pandemic and going beyond their day-to-day remit to support their customers. We hope that the key activities laid out above will help to shape next steps in the industry response, so that customers, employees, society and banks can all emerge stronger.