This article was first published by BRINK on April 9, 2019, and updated to add more information from Mercer’s report “Investing in a Time of Climate Change: The Sequel”

Institutional investors of all stripes – from those responsible for paying pensions or endowment grants, to those providing wealth management products – collectively manage trillions of dollars globally. They each have varying objectives and portfolio allocations, and function within different regulatory requirements and contexts. However, they are typically true long-term investors, allocating across the global economy to deliver returns to members, beneficiaries, and stakeholders over multiple years or decades.

Recently, evidence has grown to demonstrate that there are substantial climate-related financial implications for investors. The planet has already experienced around 1°C of average warming above preindustrial levels, and extraordinary weather events with significant financial and human consequences are increasing in frequency. Such developments make it essential for investors to address in the short term both the potential impacts of a low-carbon transition as well as the physical damages associated with climate change in order to better prepare climate-resilient portfolios for the future. Financial regulators are increasingly formalizing the expectation that investors consider the materiality of climate-related risks and manage them as part of their fiduciary duties – particularly for pension funds.

Two key elements necessitate this fiduciary duty alignment: financial materiality and growing legal and regulatory consensus.

1. Financial materiality

Technology and policy changes will be necessary – and are, to some extent, already underway – to transform the economy away from fossil fuels and mitigate additional temperature increases. This transition will necessarily open up certain companies and industries to increased risk. The financial implications most naturally point to the energy sector, but transformative change will invariably have significant implications for all energy-dependent and high-emitting sectors of the economy.

Physical risk captures the damages that come with temperature rise. The frequency of storms, wildfires, and floods will shift, as will the availability of natural resources such as water. The willingness and ability of society to adapt to these changes is uncertain. Investors with real asset exposures, such as property (held directly or indirectly) or agriculture, will increasingly need to review insurance coverage and uninsured loss implications together with additional capital expenditure requirements.

The expected financial materiality of these risks is evidenced in Mercer’s 2015 Investing in a Time of Climate Change report and in the sequel released last year. It is supported in reports by the Bank of England, the G-20 Financial Stability Board, and the Economist Intelligence Unit, as well as an increasing number of other investment-industry participant reports on recommended actions.

The findings in the sequel report particularly support the view that it is in investors’ best interests –and therefore consistent with fiduciary duty – to actively support the low-carbon transition. This means avoiding climate scenarios with the worst physical damages, which will have almost entirely negative impacts across sectors and asset classes. Even just through 2030, the portfolios modeled in the sequel (invested across multiple asset classes) could experience additional return impacts of between +0.29 percent per annum and -0.08 percent per annum, depending on the scenario and the exposures within equities and infrastructure in particular.

Financial regulators have indicated that many investors will need to consider climate-related risks in order to comply with their existing fiduciary duties

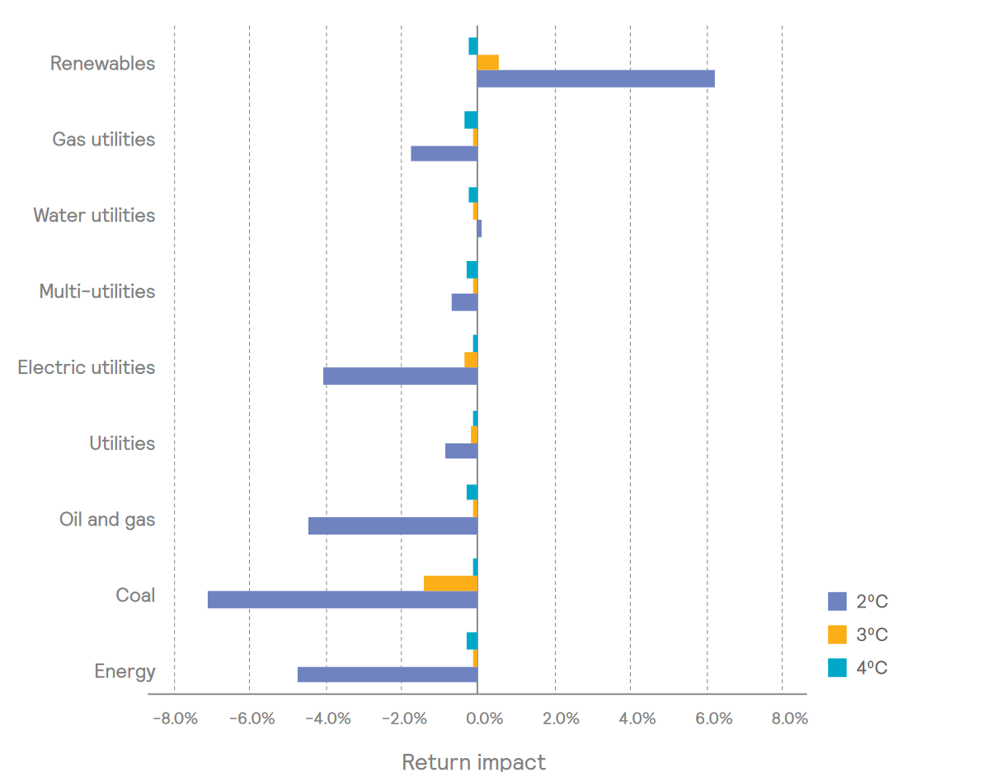

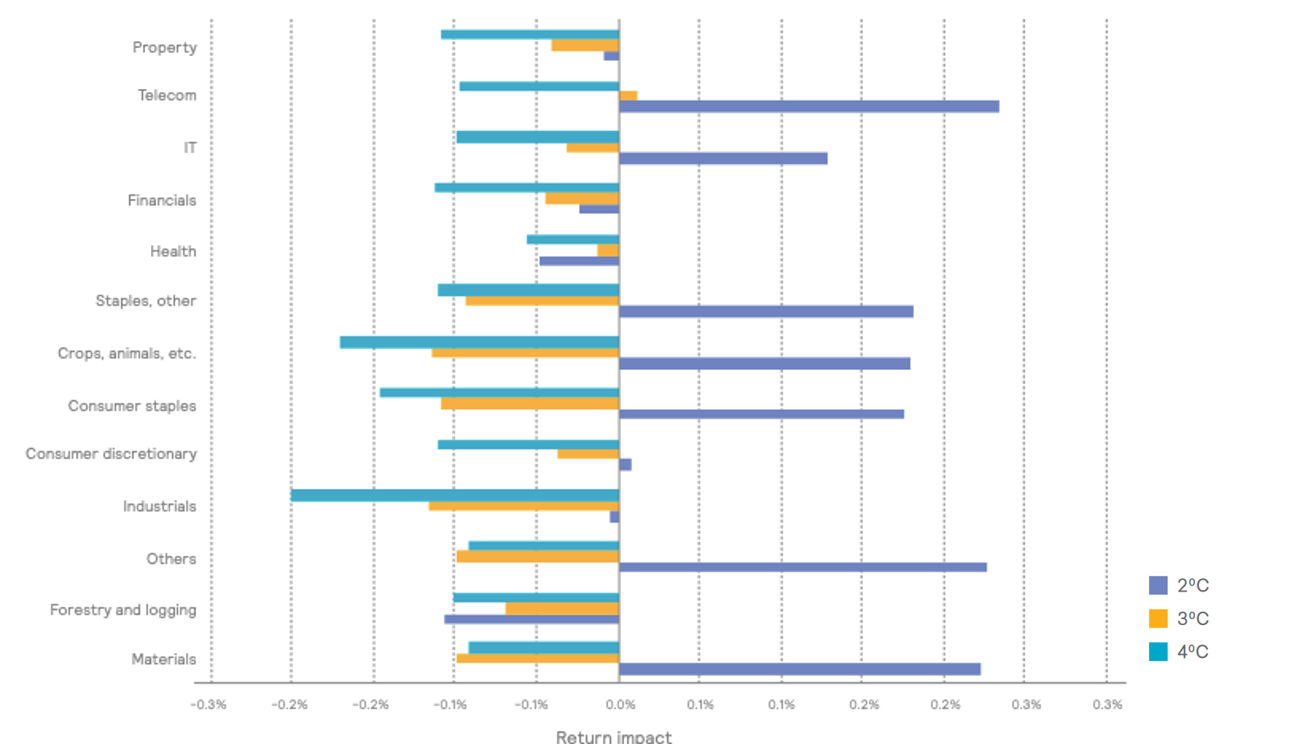

Expected annual return impacts remain most visible at an industry-sector level, and Mercer’s sequel report discusses the significant return variations that can take place in various climate scenarios. (See Exhibit 1.) For instance, a 2°C scenario by 2030 would lead to slight positive impacts for materials, IT, and consumer-staples sectors. However, in both 3°C and 4°C scenarios, all sectors have negative return impacts through to 2030.

Exhibit 1: Sector-level return impacts to 2030 (Energy and utilities sectors)

(Source: Investing in a Time of Climate Change: The Sequel)

Exhibit 2: Sector-level return impacts to 2030 (All other sectors)

(Source: Investing in a Time of Climate Change: The Sequel)

Return impacts, however, are unlikely to be neat and annualized. They are more likely to manifest as a sudden surprise. Stress testing portfolios for changes in view of scenario probability, market awareness, and physical damage impacts can help investors effectively prepare for this eventuality. Investors will then be better positioned to consider how longer-term return impacts, which may appear small on an annual basis, could emerge as more meaningful shorter-term market repricing events. Stress testing an increased probability of a 2°C scenario or a 4°C scenario with greater market awareness results in between +3 percent and -3 percent return impacts in less than a year for these same well-diversified portfolios.

2. The growing legal and regulatory consensus

As awareness of the financial materiality of climate-related factors has increased, financial regulators in a number of jurisdictions have indicated that many investors will need to consider and manage climate-related risks in order to comply with their existing fiduciary duties. In the UK, for example, a 2018 paper by law firm Pinsent Masons neatly summarizes the fiduciary duty debate in recent years and how the absence of legislation and case law has led to the focus on financial materiality and fiduciary duty. The paper concludes that “in cases where climate change has the potential to impact on long-term investment performance, pension scheme trustees have a fiduciary duty to consider climate change risk when making their investment decisions.”

The legal argument has been strengthened by recent pension-fund guidance and legislation. Europe, in particular, recognizes the potential for financial materiality and requires climate change to be considered in investment decisions, consistent with the time frames of beneficiaries. For example, the 2016 EU directive on institutions for occupational retirement provision and the UK’s Department for Work and Pensions 2018 Response on clarifying and strengthening trustees’ investment duties.

Regulatory activity has also extended across the Atlantic, with the provincial government in Ontario, Canada, requiring pensions to disclose in their statements of investment policies and procedures whether environmental, social, and governance factors are considered and, if so, how. And, in California, the insurance regulator requires insurers to disclose their fossil fuel-related holdings.

In a number of other countries, particularly in Europe, laws are also being changed to explicitly require investors to consider and disclose management of climate change-related risks. For example, the French Energy Transition Law, Article 173 and the more recent introduction of the Sustainable Finance Action Plan and the Shareholder Rights Directive, which encourage greater consideration and disclosure of environmental risks. The China Securities and Regulatory Commission issued guidelines requiring listed heavy polluters to give more specific information on emissions, with all listed firms to disclose environmental impact information by the end of 2020.

Laws and litigation related to climate change also continue to develop. Litigation is primarily being targeted at companies for failure to mitigate, adapt, or disclose, but there are examples of litigation against governments and, most recently, pension funds. In Australia, a student is suing the government for failure to disclose climate change-related investment risks for government bonds.

Signals from regulators are becoming stronger, and more investors are taking action. Those who fail to consider, manage, and disclose their potential portfolio-specific risks may be susceptible to legal challenges in the future.

In summary, forward-looking investors need to include environmental, social, and governance (ESG) factors in investment decisions, with an explicit approach to climate-change transition and physical risks, which are portfolio-wide. The transformative economic transition required to achieve 2°C and, ideally, 1.5°C, cannot be underestimated. The longer the delay by investors, along with companies and policymakers, the less likely we will attain the target of well below 2°C. The transition to a low-carbon economy will be even more difficult and disruptive.

Supporting a well-below 2°C scenario outcome through investment decisions and engagement activities will most likely provide the economic and investment environment necessary to pay pensions, endowment grants, and insurance claims over the timeframes required by beneficiaries. As the world builds a pathway to decarbonization, Mercer is ready to help investors create their own transition plans.